CFNB Year-End Review

42% upside to unlock in 2026

California First Leasing Corporation (CFNB) trades at ~70% of NAV, offering a deeply discounted entry to a liquid, diversified portfolio.

CFNB is on the verge of a short-form merger, potentially unlocking NAV value for minority holders in 2026, mirroring recent FLFG deal dynamics.

Major holdings include MSFT (~7% of portfolio), AVGO, JPM, AAPL, and NVDA, all available at significant discounts via CFNB shares.

Shares are a strong buy under $30, and a steal under $25, with a near-term catalyst from a potential go-private transaction.

California First Leasing Corporation (CFNB) is essentially a family office masquerading as a public company. It is the most undervalued way to buy a diversified portfolio at a huge discount before that discount could get unlocked in a high speed and low risk deal. Now’s the time to act. Here’s why.

The controlling shareholder is only a few shares away from exceeding 90% ownership. They have announced a self-tender, but could pivot to simply buying a few shares in the open market. After that, they could do a short-form merger at NAV similar to the recently announced Federal Life Group (FLFG) deal which will pay minority holders an over 60% premium in less than a month. CFNB can do the same. They should do the same. Next year they probably will.

Today, CFNB shares trade at ~70% of net asset value and that NAV is so liquid that it could be liquidated within minutes without an impact on prices. You can own this portfolio indirectly then profit if it goes private next year.

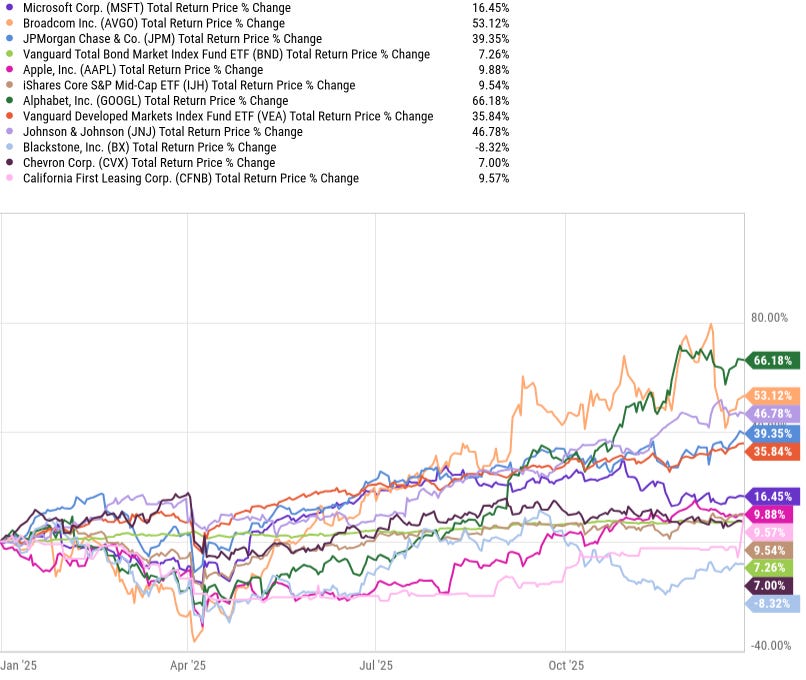

Their largest position, Microsoft (MSFT), is ~7% of the portfolio. It is up ~36% from their net purchase price. According to Microsoft Positioned For Strong Growth, Microsoft has less antitrust exposure than its megacap tech peers, a diversified portfolio well positioned for AI, and a reasonably valued stock with a P/E of ~30x. As of this writing, shares cost ~$487, but if you buy it indirectly via CFNB, you’re paying $341 per share which is less than its 2025 intraday low of ~$343 back in April.

Behind MSFT, their ten largest positions include AVGO, JPM, BND, AAPL, IJH, GOOGL, VEA, JNJ, BX, and CVX. Everything else is under 2% of the portfolio. It is a random hodgepodge demonstrating no stock picking skill, but it is good enough in a bull market and all easy to sell. By buying CFNB instead of the portfolio’s components, you get AAPL for ~$192 per share and NVDA for ~$134 per share.

Caveat

Management is overpaid relative to the modest job of managing ~$30 million of outside capital by buying well known stocks that anyone could easily just buy themselves. It is bad for us because shareholders are footing the bill for high comp. But it is also bad for CEO Patrick Paddon because it is tax inefficient to get a high salary (especially in a high tax state).

Conclusion

Most or all of CFNB’s share value could get unlocked in 2026. It is worth buying under $30 and is a steal under $25.

TL; DR

I own CFNB; you might want to buy at least a few shares, too.