Dry Powder

Time to store enough

Disclaimer / Disclosure long BRK.A, PL, TMQ, OMEX, BOXX

The way to get really rich is to have $10 million sitting in your checking account so that when a great opportunity comes along, you can act.

- Charlie Munger

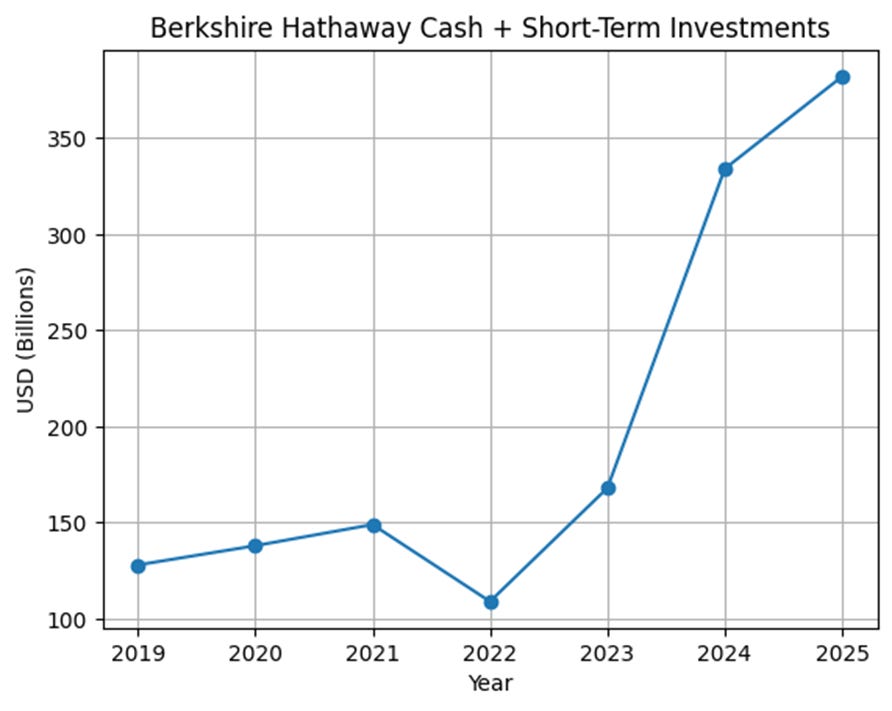

Berkshire Hathaway (BRK.A) (BRK.B) listened to Charlie with over $382 billion in cash and short-term investments such as U.S. Treasuries. They’re ready to act when a great opportunity comes along. I am at least 90% sure that there will be great opportunities in the next five years. Many of those, probably the vast majority, are not yet ripe today. So get ready. Store dry power. If not $10 million, then put $2 million aside to keep up with inflation but otherwise ready for future deployment. If not $2 million, then everyone should have at least $100k.

This is an emergency fund for financial emergencies, which can be positive or negative. It might be a crisis or an opportunity but both are urgent needs for fresh capital. Have some. How much? More than your marginal counterparty at times when liquidity dries up. On the most panicked days, you want to be on offense. If you’re on defense then your preparations failed you. The easiest financial analysis that you’ll ever do is when you’re dealing with forced selling and have new capital.

Now’s the time to store dry powder. The Buffett indicator of market cap to GDP sits at ~224%, showing a significantly overvalued US equity market likely to offer a negative total return from current prices.

We are currently in the second year of the presidential term, which is the historically weakest, returning ~3% on average, less than half as much as the second weakest year in the cycle.

The Shiller PE ratio is ~41, 49% higher than its 20-year average of ~27. Technology stocks are especially high at ~64. Tech is now over 30% of the US market cap, which is a level at which prior sector leaders have aggressively mean reverted. As a country market, the US is far more expensive than alternatives such as the UK.

The S&P VIX Index is helpful for monitoring complacency. I like looking to write optionality when it is over 30 and to buy optionality when it is under 15. As of this writing it is at 14.91.

GMO forecasts 7-year asset class returns, most recently showing the categories most likely to perform badly are US small caps at -3.6% and US large caps at -6%. I don’t think of that as a prediction as much as a possibility that I want to be prepared for. But I want my preparation to at least keep up with inflation, which is currently running ~3% per year.

Subjectively, the mood among investors appears euphoric on average. In my portfolio, the most speculative positions are doing the best with Planet Labs (PL) up 636%, Trilogy Metals (TMQ) up 389%, and Odyssey Marine (OMEX) up 219% over the past year. I’m happy with those but queasy that such positions have raced so far ahead of less speculative names.

A whole generation of retail investors have been well rewarded for being leveraged long and buying every dip. That could end badly. It makes me less excited about the long side (due to retail pushing prices up so much already) and the short side (because anything can meme and often the dumber the memier).

If Berkshire has $382 billion of dry powder and Charlie suggested $10 million, you should have $2 million. Only if that is literally impossible should you be less liquid than that today. Less than $100k leaves you extremely vulnerable to getting carried out in the next crisis and then missing the resulting opportunities.

Last year I wrote that when it comes to an emergency fund, six months is okay but one year is better,

What are your family’s combined annual expenses? This may be difficult to calculate. Rely on hard data such as last year’s credit card bills instead of your intuition because a lot of people lie to themselves about spending. You should have six months (a year is better but six months is okay) of cash in an emergency account that is not used for anything ever other than funds in an emergency. This should be in a federally insured bank account or short-term T Bill fund (mine is here). The interest rate does not matter much. What matters is that it is there if you need it. This priority comes ahead of any taxable investments. If you’ve already checked off dealing with debt, frugality, and tax-advantaged accounts, this could be the first hole in your planning.

What do I look for in an ideal emergency fund account? Principal protection from federal insurance, tax efficiency, and a high yield. I always keep such accounts within the $250k federal insurance or $500k for joint accounts. I also love to fully exploit sign up bonuses where available.

The criteria for a dry powder fund for financial emergencies is the same: low cost, tax efficient principal protection with enough yield to keep up with inflation. Here’s how I do it:

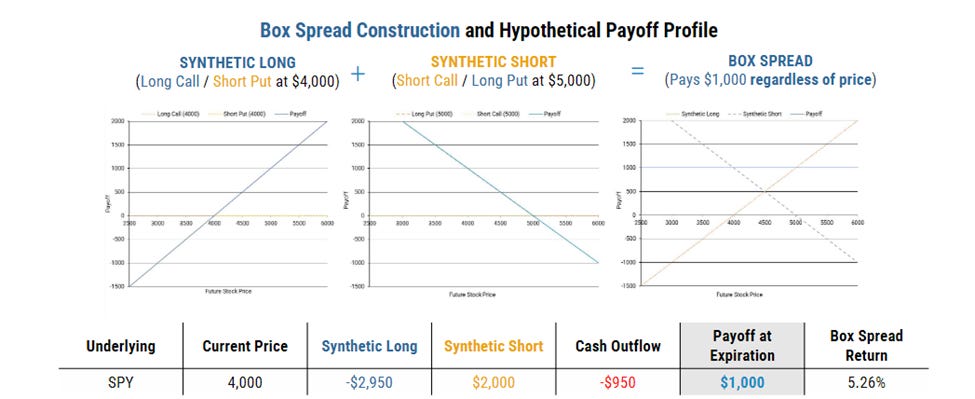

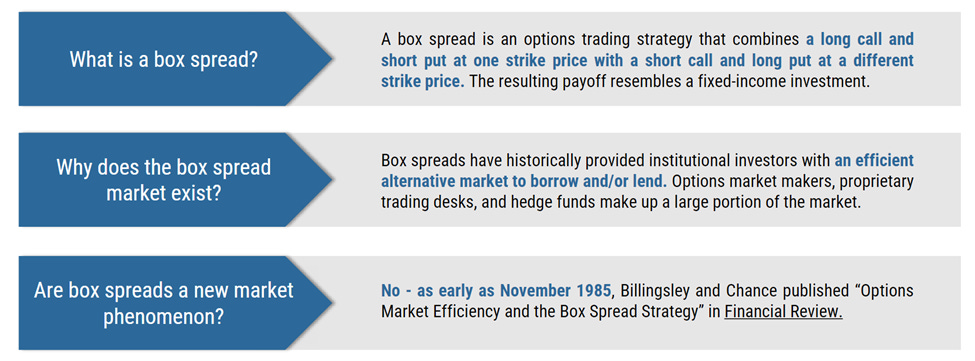

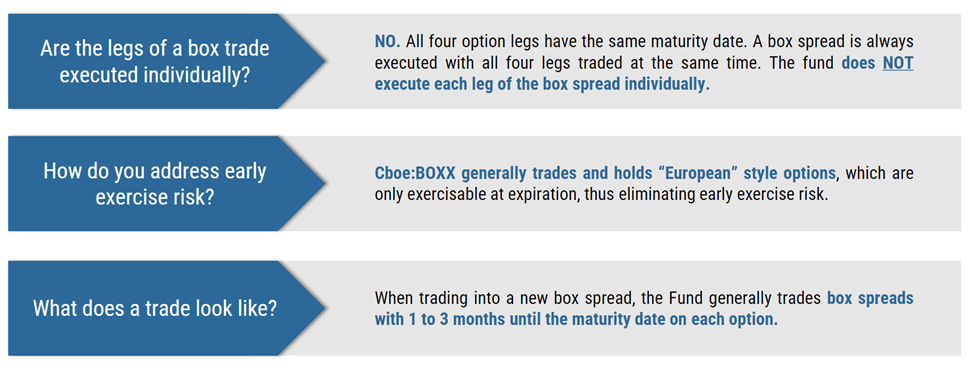

$2 million in Alpha Architect 1-3 Month Box ETF (BOXX). According to the ETF sponsor, BOXX seeks to democratize access to the box spread market, an alternative lending market common among institutional investors. The management team has done this for many years but only more recently offered it in a convenient ETF. Costs are low and tax efficiency is terrific. TL; DR: t billish yield without taxable distributions. Either know how to do sophisticated box spreads yourself for both yield and borrowing or have Alpha Architect do it for you for a ~0.19% expense ratio.

The average yield to options expiration is currently a variable ~4%, which is just enough to combat inflation. It serves its purpose of being ready for future opportunities but is only good not great. Now let’s make it great.

Get a 4% deposit match. Unlike a lot of fun but small promo gimmicks, this one has some real scale (and if you’re married you can double it by each doing it in separate accounts). Through the end of Q1, you can deposit $2 million per account or $4 million per couple to get $80k per account / $160k per family. If you are only able to do this smaller, you can get $40k for $1 million or $4k for $100k deposits. The bonus payments are made in six installments over the next five years.

This is a simple and passive prep for future opportunities that will be undemanding of the broker. Simply hold BOXX over the next five years and collect the bonus payments as you wait for fat pitches. I’ll be on the lookout; make sure you’re ready to profit from them when they come.