Long Ruger

As a customer and investor

Disclaimer / Disclosure long RGR (if the title was unclear)

December 4, 2025

I regularly visited the Ruger office and former factory near my home in Connecticut where my friend and gunsmith Mitch Schultz worked his magic for decades until his recent retirement this past year.

Mitch could look at a firearm, then look at you, and determine exactly what needed to be done. He cut down my firearms to my preferred length, lightened the triggers, then honed and polished the internal mechanisms until they performed far better than anything out of the box. The craftsmanship was sublime and the experience something from another era. When Mitch was done, if I missed with it then it was my fault.

I don’t own many Rugers but respect the brand. Their 10/22 is a good second rifle after one graduates from the Crickett. Besides that one, I have something else I prefer in every other category but they come at higher, often much higher, prices. For non-fanatics, Ruger offers solid firearms at reasonable prices with far bigger markets than premium specialty firearms.

What everyone needs: everyone capable of handling firearms safely should have a concealed carry license to be able to legally carry a compact 9 mm such as Ruger’s Max-9. It is a standard military round that is both relatively inexpensive and widely available. A pistol caliber carbine is an excellent home defense weapon in that it allows one to standardize ammo and is easy for most family members.

Beretta is also a solid firearms manufacturer. I particularly like their shotguns such as their reliable and effective A300 12 gauge. This is another firearm that everyone needs. The major caveat is that it is heavy, especially loaded with eight rounds. I personally find it comfortable, but many women and smaller framed men find its weight and recoil less so. If a weapon isn’t easy to shoot, one will train less and follow up less accurately, which is why I’m such a fan of 9 mm carbines for families.

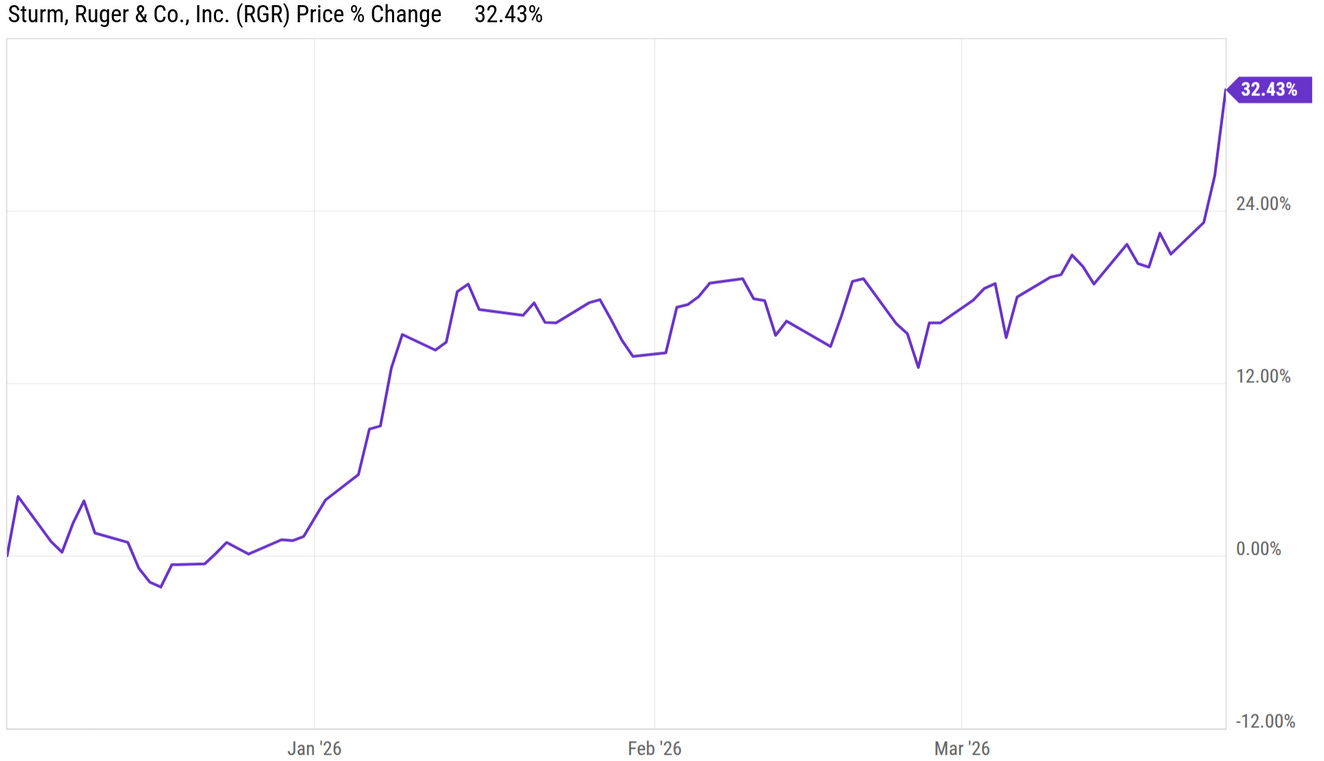

Beretta bought just under 10% of RGR worth ~$60 million and filed a 13D in which they advocate for a strategic review. Implicitly, Beretta appears eager to buy RGR. Earlier this quarter, RGR adopted a poison pill to prevent Beretta from adding to their stake. RGR had offered Beretta a standstill agreement which Beretta declined. Beretta could pay ~$50 per share for RGR within the next year.

There are few publicly traded firearms companies. It is mostly just RGR and Smith & Wesson (SWBI). My favorite firearm in S&W’s lineup is their S&W500 which chambers the 500 S&W magnum round. It is good to carry if you’re camping around grizzly or polar bears. It is better than nothing and lighter rounds would be nearly hopeless. But I have still been given the friendly advice to “save the last round for yourself”.

If there is any social unrest, firearm stocks could rally but investors will have few choices (and fewer if Beretta buys RGR). That could magnify the impact on those available such as SWBI.

A gunfight is not primarily about a gun; it is about a fight. Training is far more important than what specific firearm you use. Happily training is fun.

It is sensible to own all kinds of insurance. However, some things you need to self-insure. You are responsible for responding to violent criminals and home intruders. You are responsible for your and your family’s survival in any civil unrest. Such things may never happen, which would be great. But my home has never caught fire and I still have adequate fire insurance.

Preening and inane “ESG” investing criteria has driven many investors away from the few remaining firearms companies. Many potential buyers would not want to own RGR for political or ideological reasons. But Beretta is an optimal strategic bidder that could pay a big premium and is already in the business so wouldn’t be taking on a new political headache.

Aim small/miss small.

March 25, 2026

If you’re on the east coast and looking to improve your shooting, two venues worth a visit are the Sawmill in the south and the Sig Sauer Academy in the north.

Beretta Cash Partial Tender Offer for RGR

Proposes All-Cash Partial Tender Offer for Up to 20.05% of Shares, Providing Ruger Shareholders an Opportunity for Liquidity at a Significant Premium of ~20% to the 60 Day Average Price

Requests Exemption from Shareholder Rights Plan to Acquire Up to 30% of the Shares

Believes Increased Ownership Would Establish Strategic Partnership to Improve Ruger’s Operational and Financial Performance

Underscores 30% Beneficial Ownership Does Not Amount to De Facto Control

Beretta Holding S.A. (“Beretta Holding”), a family-owned group leading the global premium light firearms, optics and ammunition industry and the largest shareholder of Sturm, Ruger & Company, Inc. (“Ruger” or the “Company”), with 9.95% ownership of the Company’s outstanding common stock, today sent a letter to the Ruger Board of Directors (the “Board”) regarding a potential partial tender offer for up to 20.05% of the outstanding shares of the Company it does not already own at a purchase price of $44.80 per share in cash, representing a significant premium of approximately 20% to the 60-day average price (VWAP).

From the outset, Beretta Holding has been clear about the desire to make a more meaningful investment in the Company, further enhancing alignment with all shareholders; however, the Ruger Board responded by immediately and defensively standing in the way. Beretta Holding has asked the Board, in accordance with its fiduciary duties, to grant an exemption to the Company’s “poison pill” rights plan adopted on October 14, 2025, to allow Beretta Holding to acquire beneficial ownership of up to 30% of the outstanding shares of the Company by way of a premium tender offer – providing shareholders with the opportunity to decide for themselves. Beretta Holding firmly believes that shareholders deserve to determine whether they want to partner with a highly aligned, long-term strategic investor with deep industry expertise, or maintain the status quo under a Board whose members collectively own less than 1% of the Company’s outstanding shares and whose tenure has coincided with significant value deterioration.

Beretta Holding has constantly sought to engage in constructive, good faith discussions with the Ruger Board and remains open to continued dialogue in the best interests of both companies and their stakeholders.

Contrary to certain portrayals, Beretta Holding cannot be considered as a direct competitor of Ruger within the U.S. market. The majority of its sales in the U.S. are focused on shotguns and related products, as well as ammunition and optics. While the group and its subsidiaries also offer rifles and pistols, these categories represent a relatively minor portion of its U.S. business. Furthermore, within the rifle and pistol segments, the Group’s products are positioned differently from those offered by Ruger, and as such, they are not direct competitors in these areas.