What Actually Matters

Update on favorites

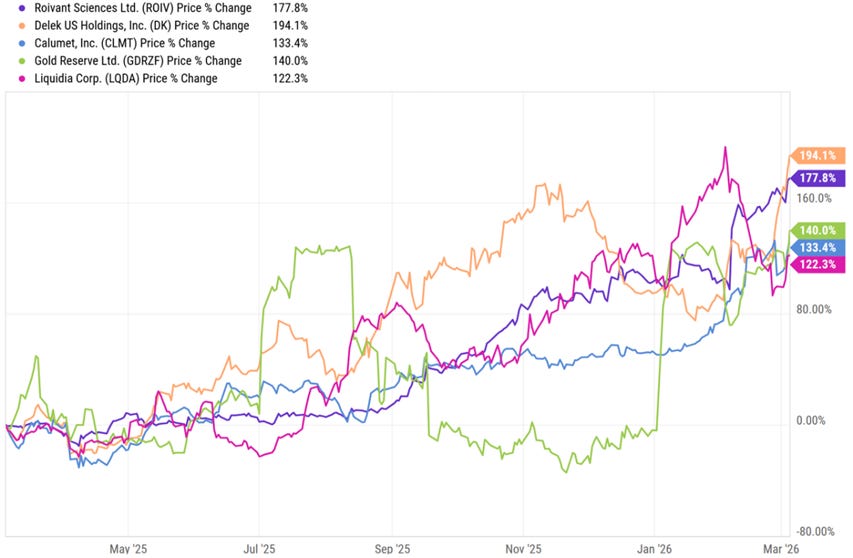

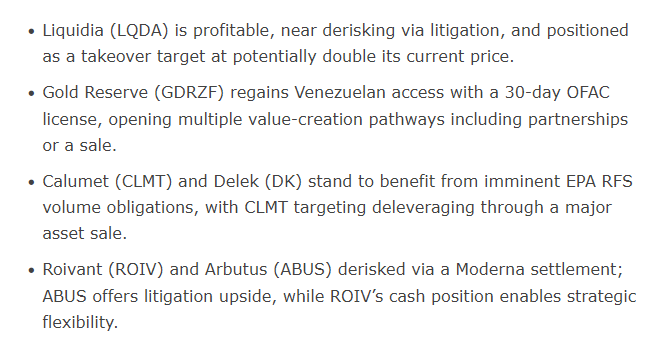

What actually matters over the past year? Liquidia (LQDA) is on the market, profitable, and awaits a single last litigation hurdle before it is a derisked, simplified takeover target for twice today’s price. A year ago the market had fallen into a hole; LQDA is up over 100% since but still has a long way to got between today and its value to a strategic buyer. I’m in constant contact with management. I’ve offered additional capital but at this point LQDA doesn’t need it and won’t.

Gold Reserve (GDRZF) is returning to Venezuela. It is no longer reliant on the Citgo sale process. The U.S. Treasury Department’s OFAC issued a 30-day license allowing GDRZF to negotiate with the Venezuelan government to return to operations in its mines. This one will require additional capital either in raises, partnerships, or an outright sale to a gold major. GDRZF has many ways to win; meanwhile there is demand for Venezuelan exposure without a lot of supply for securities.

Calumet (CLMT) and Delek (DK) could both benefit from the imminent release of the EPA’s Renewable Fuel Standard (RFS) volume obligations (RVO) this coming week. DK cost less than nothing net of its public subsidiary a year ago; the market has since started to impute value to its refineries. The RVO clarity should help more. CLMT should be able to deleverage its balance sheet with a major asset sale sometime this year. It was a leveraged equity stub a year ago and is increasingly a normal company.

Roivant (ROIV)/Arbutus (ABUS) derisked with a Moderna (MRNA) settlement this past week. The big target, Pfizer (PFE), remains. Other projects have worked so well at ROIV that ABUS has become the peppier way to play the litigation from today’s prices. ROIV is so flush with cash that a side quest could be taking a look at their Immunovant (IMVT) as a Roivant takeover candidate. I am happy with what I paid for these securities, happy with what I think I will get, and meanwhile see no need for any dramatic trades.